Dear Subscriber,

Welcome to the ninth edition of our “West Side Real Estate Market Bulletin”, featuring this month’s major issues:

- The Fed’s dilemma of lowering interest rates from today’s rate of about 7% to 2-3% while growing the economy at the same time, a contrary objective.

- The status and outlook for inflation in our local market.

- The status and outlook for mortgage rates in our local market.

Market Summary

- Although some progress has been made, our inflation rate remains high at around 6.5% and continues to constrain consumer purchasing power (See “Inflation” graph below).

- Some progress also has been made in reducing mortgage rates from a high in October of about 7% to today’s rate of about 6% (See “30 Yr Fixed Rate” graph below).

- Because of these improvements real estate buyers and sellers are more hopeful that a recession can be avoided but remain reluctant to commit resources until more positive evidence occurs.

- The labor market is showing strength with impressive growth and low unemployment.

- GDP growth has been modest because of pandemic constraints and actually was negative in the last measurement period, increasing the likelihood of a recession.

Inflation

- In a strategy to reduce inflation, the Fed has hiked interest rates up five times, albeit at a smaller increment in the last round, and predicted further similarly small increases until inflation is reduced to target levels. But what will be the impact on GDP?

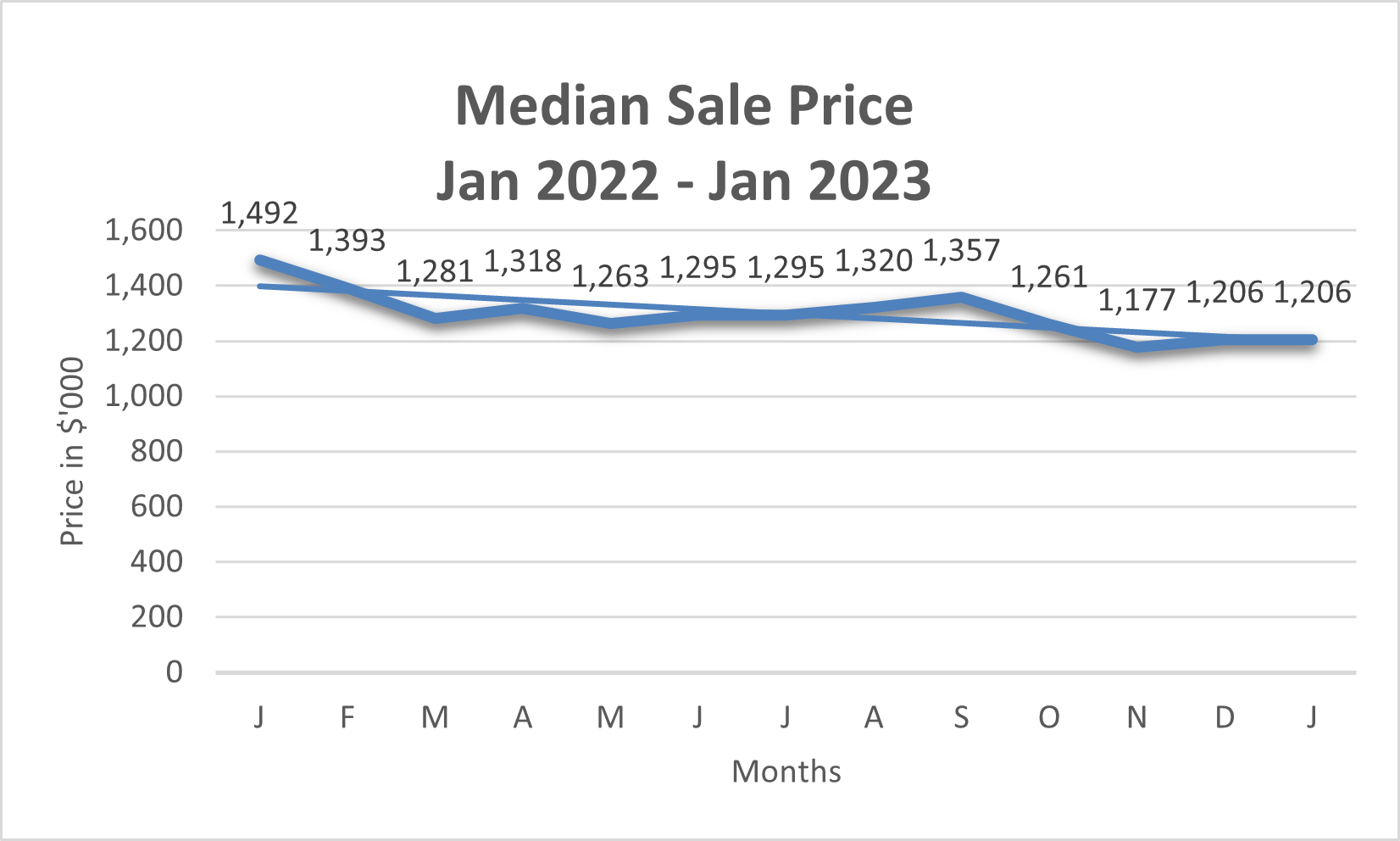

Prices and Sales Performance Prices and sales of apartment units have languished over the past year showing virtually no movement except for seasonal adjustments, confirming the prevalence of a buyer’s market. Graphs of “Median Sale Price” and “Open Listings – Supply” quantify these trends.

Thanks very much for your interest, and stay tuned!