Click the above image to see video commentary

Sponsored Content

Geopolitical factors seem to have delayed our Spring season; consequently, we are likely to see it stretch a bit further into June than usual. We’re seeing robust, but not frenzied, demand while simultaneously seeing a seasonal bump in inventory, which reveals a sense of fairness. For buyers, from a seasonal perspective, there have been more choices than in the past few years, and for sellers, there is enough interest to get the job done. But on both sides, there are caveats: For sellers, you have to be well-priced and well presented; buyers are very discriminating, and your property has to be prepared for the market to generate that appeal. For buyers, you still have to be ultimately prepared, as it is still competitive.

The most certain dynamic is that a good product commands attention. For a seller, that means staging your property, detailing it… whatever is necessary. Don’t find out that you “should have” staged and try to regroup later, as you will have lost a lot of time, money, and leverage. The old adage that you have only one chance to make a first impression is true. You should also know that your best buyers are always at the onset. In every segment of the marketplace (whether it be a studio, townhouse, luxury condo…you name it), there is a cluster of buyers out there who’ve seen every property in that category; when a new property comes on, they all go see it…you have a bit of a surge. These are the ones who actually understand value, as they are educated on the marketplace. They might also be the ones who have lost out on two other bidding wars and are willing to be aggressive. This is the Goldilocks period when you can seize your best deal; this is when the sense of urgency and competitiveness (supply & demand) peak. After just a few weeks, your price begins to erode. So you must be prepared to receive this group from the onset. Note: if your traffic is slow, you are probably overpriced; if no one is coming, you are grossly overpriced, and you missed your market. Act quickly and adjust the price.

healthier than the last few springs, activity is still sitting near the middle of the long-term historical range, not at

boom-time levels. The surprise is the staying power—this spring’s demand arrived late, but it may also linger later

into summer.

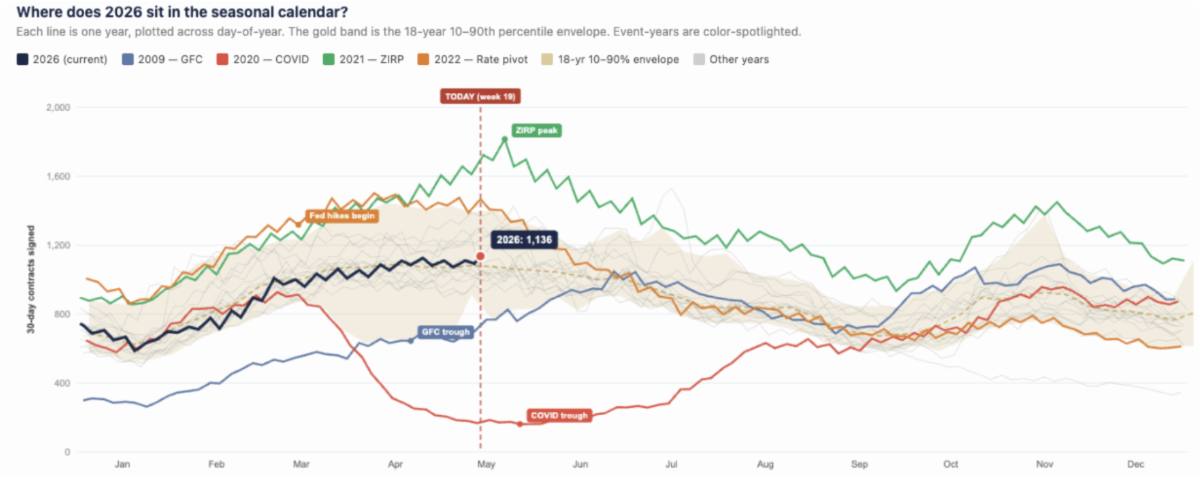

This chart compares 2026 liquidity to every year since 2008. The takeaway: while today’s market feels much

healthier than the last few springs, activity is still sitting near the middle of the long-term historical range, not at

boom-time levels. The surprise is the staying power—this spring’s demand arrived late, but it may also linger later

into summer.

Chart Courtesy of: UrbanDigs

What all of this should tell buyers (and sellers) is that well-priced, presented, and positioned properties do not last long. Our marketplace has a quiet strength that favors informed decisions and clean, compelling listings. On a macro level and layered on top of the geopolitical, there is upward pressure on interest rates and policy uncertainty, as in 2019, including a proposed pied-à-terre tax and a new 1% surcharge on all-cash purchases above $1 million. Now the specifics and the implementation (not to mention the creative workarounds that buyers will come up with) are to be determined. What’s clear right now is that buyers remain determined, sellers are more realistic, and Manhattan’s unwavering scarcity hasn’t changed. In this environment, those who engage in today’s markets thoughtfully are likely to look smart in hindsight.